Matt Bruenig hopes to launch the next Leftist policy du jour with his new paper proposing a sovereign wealth fund. But unlike Medicare For All or a Federal Job Guarantee, the American Solidarity Fund would be beholden to, rather than fundamentally challenge, the current economic paradigm.

Regardless of your impression of his contentious online presence, Matt Bruenig has managed to carve out a space for himself as the voice of pragmatism and empiricism on the U.S. Left. That sort of irreverence for accepted tenets appears from the start of his new paper, “Social Wealth Fund For America,” with an excoriation of the starry eyed nostalgia for the so-called Golden Years of Capitalism. This kind of frank evaluation is something I try to practice myself. I would guess that straightforward approach is a large part of Bruenig’s appeal and why so many were interested in what his paper on a sovereign wealth fund had to say.

NYC DSA Medicare For All logo, designed by Stephanie Monohan

In my last post, I gave a straightforward but ambitious directive: “The Left needs to shake its discomfort with wielding power and build the intellectual and political synthesis to gain power.” While I did not mention it in the post (which focused instead on net neutrality), I was inspired by a hopeful shift being enacted by the Democratic Socialists of America’s (DSA) Medicare for All campaign. Those who worked on the Affordable Care Act may remember how power rarely if ever entered into the conversation. The power of health insurance corporations and powerlessness of the people were assumed, and instead the discourse focused on how to navigate these dynamics rather than disrupt or eliminate them.

While there are some who want to return to these paltry discussions, Medicare for All could be a crucial first step for the Left towards taking power. That is why I and many others have poured so much time into it, from door-to-door canvassing to work with medical debt. There’s a great groundswell of volunteers. But that is just part one of my aforementioned directive. Medicare for All will not be won solely by the Left deciding that it should take power. We also need to create the intellectual and political synthesis to make it happen. To be clear, this is not needed to fulfill the mandates of Medicare for All’s critics. They have already shown they have no qualms criticizing strawmen rather than any policy put forth by the campaign. Rather, it is needed to make sure that when we pass Medicare for All that it is an unencumbered single payer system, that it withstands constitutional challenge, and that it does not foreclose the path towards fully socialized medicine.

At the end of every seven years you shall grant a remission of debts. “This is the manner of remission: every creditor shall release what he has loaned to his neighbor; he shall not exact it of his neighbor and his brother, because the LORD’S remission has been proclaimed. -Deuteronomy 15:1-2

Debt is often portrayed like this, insurmountable garbage or an overwhelming flood. But for debt buyers, it is a valuable commodity.

A personal goal of mine in writing this blog was to do a somewhat extensive application of all of Marx’s Capital to U.S. law. That goal did not quite materialize as I got caught up in various things, but I recently started an amazing reading group through DSA’s Socialist Feminist Working Group for women and nonbinary people to read through Capital Vol. 1. Since I will be putting time into not only re-reading it but also discussing and learning from my nonbinary and sister comrades, I figure might as well apply that knowledge to the law.

So those who have read Capital know that Marx starts things off with his analysis of what a commodity is and why the nature of commodities leads to commodity fetishism. He famously (or perhaps infamously) uses the example of linen and coats for commodities. He did not pick these commodities at random: coats are a commodity that has near-universal familiarity and linen is one of its components (at least in the 19th century). They also have a clear utility: coats keep us warm and linen can be used to make clothes like coats. And they have a clear root in production through private labor: coats are tailored and linen is weaved. But this first chapter of Capital Vol. 1 is supposed to cover all commodities because of how Marx comes to his definition of the money-form.

Marx begins by describing the two values contained in commodities: use-value, the utility of a commodity in its consumption or use, and exchange value. Exchange value is derived by the relative value between two commodities, with Marx giving the example of 20 yards of linen=1 coat. Marx notes that every commodity has an extensive number of relative values, essentially as many as there are commodities in the marketplace. He explains that these other relative values are needed to really understand the value of a commodity. If, for example, whatever market fluctuations cause the exchange value of linen and coats to go up in the exact same proportion, their relative value will remain the same: 20 yards of linen=1 coat. Throw in a third commodity however and you can understand that the exchange value has gone up, i.e. 20 yards of linen=1 coat= 1 lb. of coffee > 20 yards of linen=1 coat=2 lb. of coffee.

As such, one can craft what Marx calls the general form of value by setting one commodity against all others – “the joint contribution of the whole world of commodities.” And per this relationship, society can come up with a commodity to serve as a universal equivalent. That commodity was gold. And this relationship of “direct and universal exchangeability” made gold into money. Gold’s existence as money then made its relative value towards other commodities the price form.

Now commodity fetishism is the part of this first chapter of Capital Vol. 1 that draws a lot of attention because of how present it still feels in our day-to-day lives. The deduction of money conversely seems a bit archaic: after all, we now have a fiat currency in the United States that does not rely on the gold standard. Is modern money still a commodity? Many would argue that is not: as the economist Georg Friedrich Knapp said, money is a “creature of law” rather than a commodity. It is important to recognize however, as Marxist economist Michael Roberts points out, that Marx is not writing about money throughout existence but rather money in a capitalist-commodity economy.

Roberts also notes that the state being able to create money “out of thin-air” as is done with a fiat currency is not the same thing as creating its value. He uses the example of the Great Recession to indicate that when the value of a national currency collapses that commodities’ demand increases to hoard value.

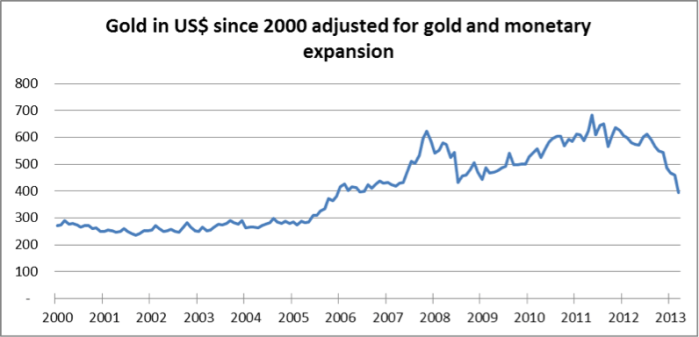

Note the spike in mid-2007 and then drop in mid-2012.

And I would argue a recent scourge of consumer protection law is also demonstrative of money’s role as a commodity and the importance of rooting the price form in relational values of exchange: the practice of buying consumer debts.

Debt buying regularly comes up in the context of so-called “zombie debt.” This “zombie debt” is debt which has been paid off but the account winds up accidentally getting bundled with a bunch of open debt accounts and sold to debt buyers. Many creditors (and we’re talking big names here like Bank of America and Discover) deal with this problem by indemnifying themselves contractually from any liability, placing the responsibility of weeding out already-paid accounts onto the debt buyers. The debt buyers in turn have little to no incentive to weed out these accounts because (1) there is literally no court in the US where default judgments are not obtained in the majority of consumer debt proceedings, and (2) the main statute protecting consumers, the Fair Debt Collection Practices Act (FDCPA), limits penalties for individual actions to $1,000. That’s less than practically any of the judgments that debt buyers stand to win from filing suit, so it is simply a matter of profit margin.

But how come companies are allowed to buy debt in the first place? People appearing in court, sued by a company they have never heard of like Portfolio Recovery or Calvary SPV, often wonder why they are dealing with some strange company rather than their original creditor. After all, the origin of our ideas of debt are mostly from Judeo-Christian concepts of morality, like the common seven year statute of limitations that can be traced back to Deuteronomy. As in prior to capitalism being the dominant economic paradigm, when the impetus of paying debts came from fearing judgment and sin. It is hard to get across to people in debt from a wide array of backgrounds that this moral system has little to no bearing on their legal proceedings. The judge probably will not, and the plaintiff will certainly not, care if someone has always “done the right thing” or made one mistake. Moral culpability is irrelevant: what matters is contractual obligation.

Debt, and its more appealing twin Credit, developed to allow for the expansion of capitalism for reasons that will be covered further into Capital Vol. 1. For the time being, it just needs to be understood that debt is a contractual money obligation by one party, the debtor, to another party, the creditor. Like any other contract, the rights it instills can generally be assigned to another party. U.C.C. 15-317. But assignment only provides a legal vehicle for the purchase of debt: what is the economic motivation? And more precisely, is debt a commodity despite being nothing other than a money obligation?

While abstracted to an extraordinary degree not even imaginable in Marx’s worst nightmares, debt is very much a commodity under modern capitalism. One element that reveals the debt’s commodity form is the difference between its use value and exchange value. Debt buyers do not purchase debts for the money owed on it. Instead, evaluating several factors (age, type of consumer transaction, attempts at collection), a price is formulated in relation to the necessary labor time needed to produce its value. This necessary labor time consists of administration, compliance, and legal collection. As such the exchange value winds up being pennies on the dollar or even less: it is literally a full-time job to track down people in debt and collect from them while complying with all the appropriate government regulations. And it should be noted that the use value of these debts is not the money owed either: debt buyers are well aware that most of these debts will settle for less than the principal and some (if people like me do their job right) may get discontinued altogether.

The example of purchasing debt shows the power of money as a concept, and particularly the price form. In any other exchange system, it would be difficult if not impossible to calculate the exchange value of a debt as a commodity with such ruthless efficiency. For starters the debt would not be for money but rather for commodities: to use an example we all can hopefully relate to, let’s say Rosa owes Lucy three tacos. Lucy decides she does not actually want the three tacos but wants to come out with something, so she tries to sell this debt to Margaret since she knows Margaret makes amazing pizza. Even assuming there was a generally recognized rate of exchange of one taco for one slice of pizza, why would Margaret risk purchasing this taco debt that she’ll then have to collect on when she could just go to someone with tacos and trade? It’s an intentionally silly example but hopefully it illustrates how complicated these relationships can be without a universal equivalent.

And of course the debt buying process is particularly interesting when we consider the debate of whether money is a commodity. Like money, debt as a contractual obligation is a “creature of law.” The obligations are not natural things but social relations. And most importantly how they relate to people (through their use value, or the collection of the debt) is different from how they relate to other commodities. The minute a price (the exchange value between money and a commodity) is placed on a debt, it relates to the entire world of commodities despite itself being an odd shadow of the very universal equivalent of money that allows this relation.

No one does crocodile smile quite like mass-evictor and current Treasury Secretary Steve Mnuchin.

Back around the time when I first started this blog, I predicted that the next president following Obama would sign into law a repeal of most, if not all, of the Dodd-Frank Act. And sure enough, with little fanfare as the media is largely focused on Russian phantoms or (more understandably) the destruction of what little public healthcare exists, the end of most of Dodd-Frank is proceeding down the legislative pipeline. Any hopes that the “populism” of a real estate mogul president would lead to tougher bank regulations is fading fast.

Mexican labor leader, internationalist, and Marxist Toledano who advocated for the nationalization of the oil industry in 1938.

As if the Western media did not have enough reasons to rally behind the right wing terrorists of the Venezuelan opposition protests, a great outcry arose from the powers that be when Venezuelan Minister of the Economy Ramon Lobo and the unions seized control of a General Motors factory to ensure that production halts are not used to further harm the already fragile economy. GM of course was not please about this development and ran to their imperialist US government for help – after all, these political friends tend to give them far more deference. Unfortunately for the auto manufacturer giant, Venezuela does not take kindly to such interventionist appeals, so GM’s assets were frozen. It should be noted that this was not some impulsive move solely stemming from the recent unrest: GM owes more than $665 million in damages to a local car dealership that is over 16 years delinquent. The Western media will of course ignore this fact despite that such an egregious violation of the law would probably even elicit an injunction from the capitalist courts of the US. Instead the focus is on nationalization, a word that conservatives and liberals alike have tried to make into a slur, especially in response to any attempts to condition the recent bailouts of the auto industry and banks on even lukewarm reforms.

The Rebellious Lawyering Conference (RebLaw) began yesterday at Yale Law School, bringing together law students, lawyers, and community organizers to discuss a plethora of social justice issues. The author attended two of the sessions, which were amazing and yielded interesting legal perspectives and strategies worth elaborating on (and of course there were many simultaneous sessions which you can check out here). And tomorrow I’ll give a similar summary of the sessions I attend today.

Things are looking worse and worse for the liberal advocates of legalism and reform as direct action continues to win over and over and over again while doing things through the proper channels continues to fail. The latest blow is the resignation of Federal Reserve Board Governor Daniel K. Tarullo. Mr. Tarullo’s term was supposed to continue until 2022 but, for undisclosed reasons, he has left prior to that expiration. Know for his rigorous (or haphazard, at least according to the bankers) stress tests that he conducted against the banks to test how they would weather various economic emergencies, Mr. Tarullo was the closest thing to a public advocate on the Fed. Admittedly not a high bar, but nevertheless with his departure things will likely get worse for the working class.

Secured transactions are transactions where payments, typically on a loan of some kind, are secured by certain goods, called collateral, being subject to seizure upon failure to make payment. Mortgages, pawnshop loans, and money judgments from a lawsuit are all examples of secured transactions. Like most kinds of financial accumulation, they are speculative – they do not have the capital and may not get the capital depending on the circumstances. That risk however is mitigated by the ability to foreclose on the collateral to the loan and subsequently liquidating or reselling it to recover some, all, or even a surplus of the money owed.

Such transactions are ones that modern orthodox economists like to point to as too complicated or too attenuated from the labor theory of value for Marxist economics to explain. This reasoning comes from a misunderstanding of the labor theory of value – Marx never asserted that capital accumulation only comes from the immediate exploitation of wage labor. But even in these transactions, the value realized can always be traced back to its creation by labor. Loans are a paradigm of the neoclassical fiction of economics: the debtor benefits from having more capital in the short term to spend and the creditor benefits from making a profit, either on the interest or on foreclosing on the collateral and reselling it (admittedly this is a gross oversimplification, but nonetheless is the core of the profit motive). It seems to be win-win. And that is certainly how these transactions are marketed to consumers:

Anything I want? Even investment centrally planned by a proletarian state?

Last night I finished Michael Roberts’s new book The Long Depression, an epic defense of Marx’s law of political economy that the tendency of the average rate of profit of capital was to fall and an argument that the world is in a long depression, the third economic depression since the rise of capitalism. Readers may recognize the author as I have often cited to the prolific work he has done on his blog, as well as recommending him to all of those who want a solidly Marxist perspective on economics. The book provides an exhaustive computation of the effect of Marx’s law, as well as refutations of a number of alternative explanations (Keynesian, neoclassical, Austrian school, monetarist, Ricardian, etc.) for the economic history of the world from 1873 until the present day. It is a fantastic book not only for Marxists eager to learn more about economics but for Marxists to share with STEM-oriented friends who are more receptive to Roberts’s quantitative focus than to the more sociological arguments for Marxism.

I knew I had to write something promoting this book but I’m at best an amateur economist, so my judgment of Roberts’s argument is not particularly useful. However, I can highlight the arguments of the book by putting forth my own supplement on how the U.S. law correlates to the economic phenomenons that Roberts describes. As the proposal to reinstate the Glass-Steagall Act emerges from the shadows it has lingered in for over a decade, it is crucial to understand how a capitalist economy works and what effect the laws have on them.

The man pictured above nervously staring down the truth that Karl Marx wrote more than 121 years ago is Lloyd Blankfein. Mr. Blankfein is the Chairman and CEO (a duality typical of modern finance) of Goldman Sachs. Despite his grim look in this picture, Mr. Blankfein has a sunny disposition nowadays despite having had “600 hours of chemo” to eradicate the cancer growing out of his lymph nodes. Supposedly he’s been cured, which I’m sure was a big relief to Democratic presidential nominee Hillary Clinton. Clinton is close to Blankfein, and to Goldman Sachs in general. While mainstream media likes to frame Gary Gensler as a “Wall Street cop,” the campaign of Bernie Sanders responded to his hiring as Chief Financial Officer of Clinton’s campaign by saying that they “won’t be taking advice on how to regulate Wall Street from a former Goldman Sachs partner [at the age of 30] and a former Treasury Department official who helped Wall Street rig the system.”

The Rebellious Lawyering Conference (RebLaw) began yesterday at Yale Law School, bringing together law students, lawyers, and community organizers to discuss a plethora of social justice issues. The author attended two of the sessions, which were amazing and yielded interesting legal perspectives and strategies worth elaborating on (and of course there were many simultaneous sessions which you can

The Rebellious Lawyering Conference (RebLaw) began yesterday at Yale Law School, bringing together law students, lawyers, and community organizers to discuss a plethora of social justice issues. The author attended two of the sessions, which were amazing and yielded interesting legal perspectives and strategies worth elaborating on (and of course there were many simultaneous sessions which you can  Things are looking worse and worse for the liberal advocates of legalism and reform as direct action continues to win

Things are looking worse and worse for the liberal advocates of legalism and reform as direct action continues to win

Last night I finished Michael Roberts’s new book

Last night I finished Michael Roberts’s new book