Matt Bruenig hopes to launch the next Leftist policy du jour with his new paper proposing a sovereign wealth fund. But unlike Medicare For All or a Federal Job Guarantee, the American Solidarity Fund would be beholden to, rather than fundamentally challenge, the current economic paradigm.

Regardless of your impression of his contentious online presence, Matt Bruenig has managed to carve out a space for himself as the voice of pragmatism and empiricism on the U.S. Left. That sort of irreverence for accepted tenets appears from the start of his new paper, “Social Wealth Fund For America,” with an excoriation of the starry eyed nostalgia for the so-called Golden Years of Capitalism. This kind of frank evaluation is something I try to practice myself. I would guess that straightforward approach is a large part of Bruenig’s appeal and why so many were interested in what his paper on a sovereign wealth fund had to say.

Mike Konczal wrote a general response to the paper which captures most of my problems with it, and a broader critique of “market socialism,” that I will try my best not to retread. There is also a lot of room to critique the notions of citizenship in Bruenig’s piece and the sort of neo-Americana aesthetic he is trying to sell the policy with. But unfortunately I’m not familiar enough with the subject to write on that aspect.

One stone left unturned however is so commonly neglected by the Left it’s worth diving into with some detail. And that’s how consumption, and particularly consumer finance, function under modern U.S. capitalism, and how failure to account for that will be a major stumbling block to ASF redistributing wealth.

Bruenig’s lodestar for a social wealth fund that also provides a universal basic income is the Alaska Permanent Fund:

What sets the APF apart from virtually all other SWFs in the world is that the APF pays an annual cash dividend to every citizen of Alaska. It is thus a homegrown model of the kind of SWF I think the federal government should implement on the national level.

The first troublesome bit of the APF is the admitted history of its creator, Governor Jay Hammond. Bruenig admits that Hammond’s first foray into SWFs was blocked until it was offered “in exchange for an elimination of the local property tax.” This political reality is something Leftist advocates of UBI try to avoid while UBI advocates like Charles Murray are very fond of.

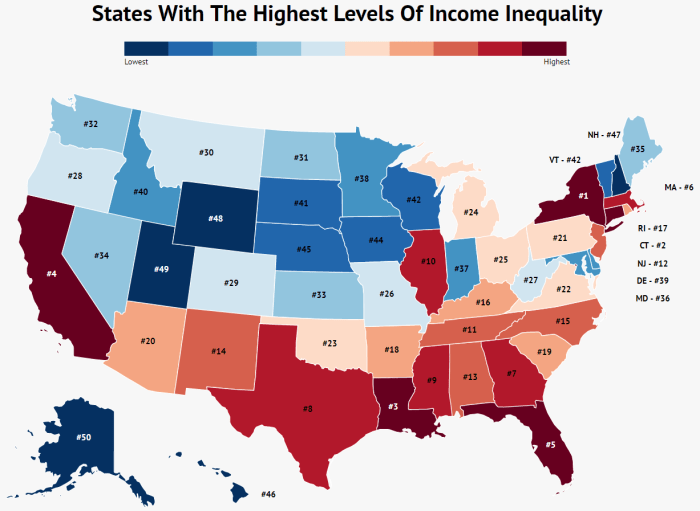

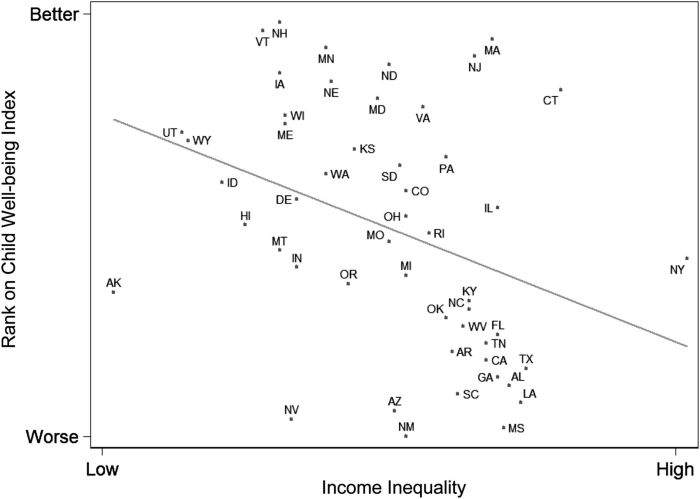

Bruenig hopes to use the example of the APF to show how successful a SWF with a dividend could be on a federal level, such as by noting that Alaska is “the most equal state in the country.” And in regards to income inequality, he is right:

But does income inequality capture broader inequality? There are reasons to believe the metric is limited particularly in situation with some kind of universal basic income.

And Bruenig’s own ASF being tailored to citizenship is particularly worrying in the context of the APF; Alaska’s poorest are disproportionately immigrants who are not eligible, at least initially, for the APF.

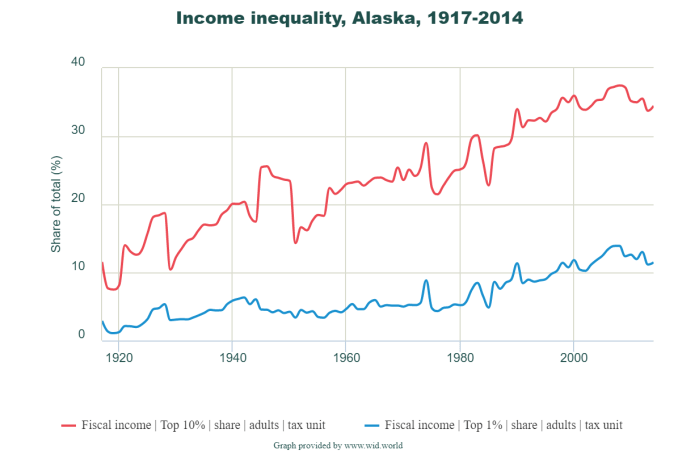

It’s also somewhat dubious that the APF is the reason for Alaska’s relatively low levels of income inequality given that the rate of increase in income inequality in the state grew after 1976. Bruenig himself hints at this when he writes that “the main drivers of the APF’s return in any given year are general economic conditions.” The share of income held by the top 10% has increased by about 60% since the APF was rolled out.

The argument could be made that even if income inequality has increased in Alaska that the APF has mitigated that increase. And there have been studies that show the APF has decreased inequality among certain demographics like indigenous people, women, and people in rural areas (and unsurprisingly indigenous women in rural areas being among the most benefited). But then the question becomes why distribute a dividend to everyone, where the results are mixed or inconclusive, rather than the people who have clearly benefited from it?

A policy of course should be judged by its own merits, not the merits of its antecedents, so I am going to cut short the analysis of the APF and move on. My main contention as to the ASF is it seems more tailored to creating a sort of masterpiece of statecraft than the best policy to deal with economic inequality. Even though, as previously noted, Bruenig uses the APF because it contains the only example of his novel approach to SWFs (a dividend), he then proceeds to spend most of the ASF proposal laying out its most mundane aspects.

He gives five ways of accumulating capital into the fund, and in regards to levies provides nine more specific ways. None of these however really require serious inquiry; I doubt anyone questions that the government can gather assets and certainly the Fannie/Freddie receivership and its legal history should put that notion to rest. Perhaps if any of the proposed means of doing so were novel, it would make sense to spend so much time on this portion but, in short, they are not. While the governance part is probably the most articulate part of Bruenig’s proposal, it again is not anything particularly new or profound. It again mostly surveys previous ideas proposed by others like Dean Baker and then Bruenig asserts which of those he would support.

Essentially the majority of Bruenig’s paper comes off more like a pitch to investors than a policy proposal for fighting inequality. He seems far more concerned with how large and well-run he could make the ASF than how effective it would be at alleviating inequality. Which brings us to the slimmest section of the proposal: how his dividend would actually operate.

Bruenig bases the ASF divided on the APF dividend with some minor adjustments. In the ASF, every citizen 18 years of age or older would receive one nontransferable share in the ASF, which entitles them to receive the UBD. Bruenig adds this aspect as, in his own words, “a communications gimmick” – to impress on the holders of ASF shares that they are truly owners of the fund as well as entitled to the UBD. The share would be tied to an app/website like Fidelity where a person could track the value of their share, learn more about the ASF’s investments, and apparently look at lots of white people (I know the last one is petty but seriously every person pictured in Bruenig’s paper is white). The distribution mechanism, the very basis of redistribution, is given one vague sentence: “This is also where they would input their banking information and address to receive their dividend checks.”

Contrary to Bruenig’s assertion, I do not believe the distribution of the aggregated wealth of the ASF in dividends is “the easiest” part. To begin with, the need for an actual share to impress upon people that they are owners seems by Bruenig’s own assessment unnecessary via the experience with the APF: “The Alaska Permanent Fund does not provide any kind of formal ownership shares, but the residents of the state nonetheless conceptualize themselves as joint owners of the fund.” And for something that is not actually needed, it creates a lot of risk for being used to dismantle, gouge, or water down Bruenig’s whole plan. The Right-wing in the U.S. can essentially repeat the story of re-commodifying housing in Cuba – they can say to people “Hey, if you truly own this, why won’t the government let you sell it? Sure you can get $3,000 this year in the dividend but I would buy your share for $10,000 right now.” You cannot, without major accompanying reforms in practically every area of the law, give someone an ownership share in something and force them not to sell it. Even if the laws were not changed to allow the sale, you would just see the rise of loans tied to UBD, similar to payday loans or tax refund loans. If the form of a benefit is literally the asset with the most liquidity, preventing it from moving will be like trying to controlling a bucking bronco.

That problem however is admittedly somewhat speculative. What is not speculative is the need for a way to get the dividend in the hands of the recipient. While the amount of the underbanked in the United State has decreased in the past ten years, eight percent of people still used check cashing services. That is why even the federal government has recently resorted to providing prepaid cards for distributions to citizens like tax refunds, Social Security, and virtually any other government benefit. The problem with prepaid cards is that unlike direct deposit (which would be handled through FedWire), they require the government partnering with private corporations. This service specifically was contracted with Comerica Bank, who then contracted with MasterCard to put out a card branded Direct Express. If you do not know people who access such benefits through that card, I would invite you to meet some of them here. Providing government benefits in the form of monetary income allows it to be more easily siphoned off through fees, and that is why Republicans have consistently pushed to move benefits towards these kind of services through legislation like the Taxpayer ID Protection and Fraud Prevention Act (the name is like “right to work,” in that it would make government benefits less secure).

But what about the majority of people who could receive the income into a bank account? That is where we get into the biggest problem with monetary income wealth redistribution: consumer debt. There’s currently $3.918 trillion in non-mortgage consumer debt. The break down of the major parts of that close to $4 trillion is $1.125 trillion in outstanding auto loans, $1.531 trillion in student loans, and $1.036 trillion in revolving credit (generally credit cards). The average household has $15,482 in outstanding credit card debt alone, about 26.22% of the median household income ($59,039). The average household holds $134,058 in total consumer debt. In other words, the average household has more debt than their household brings in in income over 27 months.

Some have criticized the recent celebrations of increased wages particularly in this context, as well as the capture of income by rent payments (now at an average of $1,405 per month). While this is certainly part of the analysis, it would not necessarily weigh against Bruenig’s dividend. More income would hypothetically mean a smaller share of total income being captured by debt and rent. Sure there would be reason to push back against, again, the use of income inequality as a metric for broader inequality but a decrease in income inequality would be an overall good.

The issue however is how much of a good it would be. An increase in income would also lead to creditors increasing what monthly payments they require, could push people off the rolls of state government benefits even if there were laws to not factor it into the means testing of federal benefits, and so on. I know I said I would avoid retreading Konczal’s critique but his words are worth repeating here: “Why not spend that trillion and a half dollars in a useful way right now?” The problem with the debt capture I have outlined is that a good amount of the dividend will not go to benefiting the public but instead to the various creditors of the average household. And if the goal is income redistribution, let alone wealth redistribution, that is a serious problem.

And this problem does not arise in all Leftist policies. You do not have this problem with Medicare For All because a creditor cannot garnish medical services (not to mention it eliminates the creation of further medical debt as I have often written about). You have this problem to some extent with a federal job guarantee, but far less than UBI for two reasons. First because wage garnishment is more limited than bank garnishment in how much the creditor can take (with a couple of exceptions I won’t get into here). Second because a job, unlike a dividend, provides far more benefits than monetary income.

It is that second reason that I believe represents the biggest divide between the proponents of a federal job guarantee and a universal basic income (including Bruenig’s dividend here). There are of course the formal benefits like health insurance, insurance, retirement, and so on. But there are collective benefits to society as well since not limiting employment to the whims of the market allows for labor-intensive projects like care for the elderly, social infrastructure construction, sustainable agriculture, and so on. UBI, including Bruenig’s dividend, relies on a “vote with your dollars” logic to produce similar benefits beyond reduction of income inequality. Funnily enough, at least one survey seems to suggest that most of the working population recognizes this even if Bruenig does not.

I am not against providing any and all monetary government benefits. However, there seems little to no reason to make them universal when cases like Alaska show they only decidedly help some populations (rather than the working class in general) and their benefit to others would be greatly mitigated by the parasitism of finance both at the point of distribution (like the prepaid benefit cards) and once the person has the benefit (absorbed by debt and rent). While socialists should support social ownership, including through social wealth funds, we should not internalize the capitalist logic that the best way to help others is to help them as consumers through a universal basic income detached from the kind of collective social benefits you would see in policies like Medicare for All or a federal job guarantee.

Thanks to all my supporters on Patreon: Brian Stegner, Sarah Jaffe, Winona Ruth, Michael Rosenbloom, Red_Rosa, John Michie, Jay Schiavone, Daniel Hafner, Aaron Marks, Eli, and my anonymous donors. For $1 a month you can join this list and support my work/help me survive bar study.

One thought on “United We Are Garnished”