People hate that I love Senator Elizabeth Warren. Which at first glance may seem surprising: after all, Warren is beloved by a large portion of the Left and even some people outside of it. But it isn’t her that’s the problem: it’s me. My liberal friends hate that I share her videos yet constantly chide and push them to be far more radical than the views she expresses. My radical friends hate that I defend her decision to not endorse Bernie Sanders, her decision to not run for president, and even her decision to be a Senator. Her sharp style of argumentation and rational, no-nonsense demeanor makes her an ideal populist candidate for a country fed up with big finance. But her and I both know that, at least at this point, she does more good as a Senator.

A recent letter that she wrote to the Securities and Exchange Commission is a great example. As part of the legislature, she is separated enough from a federal agency to write a relatively scathing critique, but still occupying a high enough position in the political hierarchy for such a critique to be taken somewhat seriously by both the agency and the mainstream media. I get the utility of that, and it’s why I’m not one of those “Grab an AK and some friends and go up to the mountains” type of Marxists. But while I don’t think what Elizabeth Warren does is useless, I try through my work to push her and others away from the Democrats and away from capitalism. Trotsky called this the transitional program. I like Elizabeth Warren because she reminds me of so many people I see in my life: my co-workers, mentors, and even students (God I’m getting old) who hold intense passion for making the world a better place, possess incredible skill sets, but are restrained by cynicism or lack of imagination to advocacy and reform. These are the people that will bring about socialism – people like me are just the ones who light the match that gets it going. And honestly, it is amazing to get to do that with so many other women when I know that people like Warren were not so fortunate when they were younger. Okay, enough feelings, on to the law!

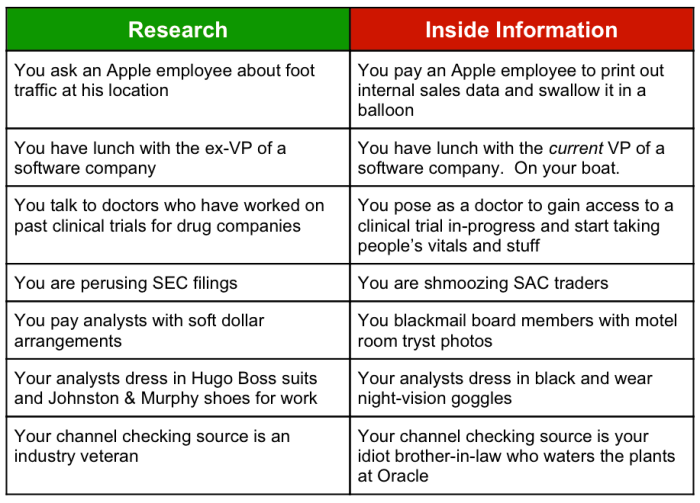

BFF Warren is mad at the SEC for approving Stamford Harbor Capital LP’s application to register as an investment adviser for outside clients. Specifically she’s mad because Stamford is the most recent venture of insider trading hedge fund manager Steven A. Cohen. Cohen was barred by the SEC just this last January from “supervising funds that manage outside money until 2018.” This injunction was the result of a joint civil and criminal investigation of his hedge fund, SAC Capital Advisors, LLC that led to the standard plea where fines and even some injunctions are doled out in exchange for the firm and individuals admitting to no wrongdoing. Note how worthwhile that no wrongdoing part is for them – these are individuals who love risk, but they almost never risk the trial even when facing 2 years of tip-toeing through legal loopholes. We’ll touch on that again more later.

Steven Cohen was found to have abetted insider trading, particularly 17 C.F.R. § 240.10b–5:

It shall be unlawful for any person, directly or indirectly, by the use of any means or instrumentality of interstate commerce, or of the mails or of any facility of any national securities exchange,(a) To employ any device, scheme, or artifice to defraud,(b) To make any untrue statement of a material fact or to omit to state a material fact necessary in order to make the statements made, in the light of the circumstances under which they were made, not misleading, or(c) To engage in any act, practice, or course of business which operates or would operate as a fraud or deceit upon any person, in connection with the purchase or sale of any security.

What is insider trading and why is it illegal? Insider trading is simply when anyone who trades in securities uses private information to make their decisions about how to purchase or sell. Securities are any note, stock, treasury stock, security future, security-based swap, bond, debenture, evidence of indebtedness, certificate of interest or participation in any profit-sharing agreement, collateral-trust certificate, preorganization certificate or subscription, transferable share, investment contract, oil and natural gas certificates, yadda yadda blah blah blah. Basically any kind of financial instrument. The SEC has four general reasons for regulating the exchange of securities: (1) a lot of the public participates in it, whether they’re aware of it or not; (2) the federal government needs to be sure of values for taxing purposes; (3) securities trading is prone to speculation which can destabilize the banking system; (4) national economic recessions and depressions are exacerbated by securities manipulation. But of course, there are the stated reasons and the actual reasons. The actual reasons are an expansion of (2) and (3).

Despite what your college roommate’s libertarian boyfriend thinks, the US and various exchange markets are in a co-dependent relationship. After all, markets need the United States government to charter corporations, enforce contracts, produce currency, and many other basic requirements. On the flipside, the United States does not accumulate much capital itself outside of dispossession, and requires markets to tax in order to exist in its current behemoth size. Insider trading destabilizes markets because if not controlled it can cause capital flight. While part of the original Securities and Exchange Act in 1934, the prohibition on insider trading did not really get enforced until the 1980’s, when global communication meant that for the first time access to “insiders” could create advantages large enough to push others out of the market.

From pharmaceuticals to natural gas, many securities are tied to heavily regulated commodities that have to pass through various stages of development, registration, etc. Let’s use the example of an oil company. Kill the Earth Inc. drills for oil in Alaska. Stock in their corporation is owned by five investors: a hedge fund and four bored retirees. Hedge funds and other financial companies are called institutional investors – while the bored retirees may have a lot of time to commit to watch CNN Money, the hedge fund has millions of dollars to throw into research, technology that can make trades in microseconds, etc. The hedge fund has an advantage, but sometimes they’ll be wrong, and more importantly when they’re right often times even the little guys will also know to make the same moves. But if Kill the Earth Inc. feeds information to the hedge fund first, for a generous consulting fee, they will almost always make profitable moves and be able push the other investors out. But institutional investors are like Tinder dates – high investment but very short term. Once they have decided for whatever reason to abandon Kill the Earth Inc., the company is destabilized because those long term investors all got pushed out.

To prove insider trading, the government can infer initial suspicion required to conduct an investigation and other administrative procedures by the trades being made in certain securities and of certain amounts, particularly when such trades contradict previous behavior, supply-demand fundamentals, etc. e.g. In re Lernout & Hauspie Securities Litigation. However, the government cannot prove insider trading just from finding private material information in the possession of the trader – they must also be able to demonstrate that they had the intent to use that information in the buying or selling of securities. U.S. v. Smith.

An employee of Steven Cohen, Mathew Martoma, had built a long position in stocks of two pharmaceutical corporations, Elan and Wyeth, over the development of a drug for the treatment of Alzheimer’s. However, a doctor who was also did consulting work with hedge funds like SAC tipped off Martoma that one of the unreleased clinical trials was not going very well. Martoma met with Cohen and insisted that they liquidate their holdings and build short positions. Martoma was prosecuted for the insider trading and found guilty, and while they did not have evidence that Cohen knew that it was insider trading, such a huge reversal should have raised red flags for him. This is further evidenced by an analyst asking Cohen why Martoma wanted to make the switch since the clinical trial results were not available yet. Cohen profited $275 million off the information from gains and prevention of losses.

Why did Cohen accept this deal rather than fight it as Martoma did and is still doing on appeal? Because Cohen is not a small-time trader like Martoma. He still has all the connections that he did before this finding, and he cannot jeopardize his ability to use them and have people invest their money with him by any official acceptance of wrongdoing on his part. For Cohen it’ll be easy enough to explain away: “I didn’t know and the SEC couldn’t even prove that I did. But I had to take that deal otherwise I’d jeopardize your money. That’s the Federal government amirite? Thanks Obama.”

The fundamental mistake in Elizabeth Warren’s analysis is that the SEC would ever be interested in protecting the public from someone like Steven Cohen. Again, they very much do want to prevent insider trading, but they also do not want to talk someone like Steven Cohen with his billions of dollars out of the market. After all, insider trading is just a necessary line in the sand: unfair advantages in the market are generally condoned. The mass exploitation of people in poverty, whether through subprime mortgages, debt trading, or destabilizing prices of important commodities like oil, is part of the system. The SEC’s mission is not to protect us – it’s to protect the markets. And that, even more than particular actions like insider trading, is the unacceptable outcome.

4 thoughts on “Unacceptable Outcomes: An Ode To Elizabeth Warren”