The Volcker Rule, also know as United States Code Section 1851, was the consolation prize for the Glass-Steagall Act failing to get reinstated. It prohibits banking entities from engaging in proprietary trading or acquiring “any equity, partnership, or other ownership interest in or sponsor a hedge fund or a private equity fund.” For Glass-Steagall Act supporters, it was viewed as too little. For those who support continuing the abolition of Glass-Steagall, such as presidential candidate Hillary Clinton, the Volcker Rule is viewed as a go-around. They want to get rid of it because the very same banking connection to proprietary trading, hedge funds, and private equity funds helped bail out these institutions during the recession. And then they, in turn, were bailed out by the federal government and other banks.

The Volcker Rule was made explicitly in recognition of this dynamic: the constituents said no more bailouts, so Congress made it impossible for bailouts to ever happen again, at least in the way they did with Bear Sterns and others. One criticism raised quite fairly is that the Volcker Rule may not actually prevent bailouts. But often it is under the delusional rationale of free-market dogmatism, rather than recognizing that a porous, watered down version of Glass-Steagall will never be a substitute, even in the short term, for the reinstatement of Glass-Steagall. Not to mention that it was only this year that the rule actually took effect, and it won’t be until next summer that we see audits to check for compliance. Until then, the effects of the rule are at best conjecture. But we do not have time: the last minute sellings of prop desks and CLO’s at least demonstrate continued interests by the banks to engage in activities prohibited by the Volcker Rule.

The most succinct but comprehensive capitalist argument against the Volcker Rule I have found was provided George W. Madison, Gary J. Cohen, William A. Shirley in the Banking and Financial Services Policy Report, entitled “Reconsidering Three Dodd-Frank Initiatives: The Volcker Rule, Limitations On Federal Reserve Section 13(3) Lending Powers, AND SIFI Threshholds” (34 No. 6 Banking & Fin. Services Pol’y Rep. 1). They divide criticisms of the Volcker Rule into four types: Risk, Liquidity, Complexity, and Competition. While they do not address Competition directly because they claim their criticisms are not concerned with it, their underlying ideology, both express and implicit, centers on competition as regulatory and I will criticize that in turn. However, because I see the questions of liquidity and complexity as being subsumed within the question of risk itself, I will in the interest of time focus solely on the arguments made about risk.

The structure of “Reconsidering…” introduces each criticism with Chairman Volcker’s rejection of similar criticisms. While I doubt the truncated summaries are not necessarily accurate representations, I do agree that Volcker’s justifications often fall short or are simply wrong. In other words, this is not me countering Madison et al’s arguments to defend Volcker’s as much as to assert options outside such a constricted binary.

The financial industry is rather torn about how to handle the criticisms of risk. Risk is far too important to their industry for them to accept changes that significantly lower risks. Let’s give a brief illustration of what risk means to finance. Before the United States’ credit rating was downgraded to AA+, U.S. Treasury bonds in a one year period were practically a risk-free investment: there should be no difference between your expected return and actual return. That looks like this:

Where is the variance curve? There is none: the actual results will always line up with expected results. Now let’s look at hedge funds, as conveniently set next to the more secure mutual funds:

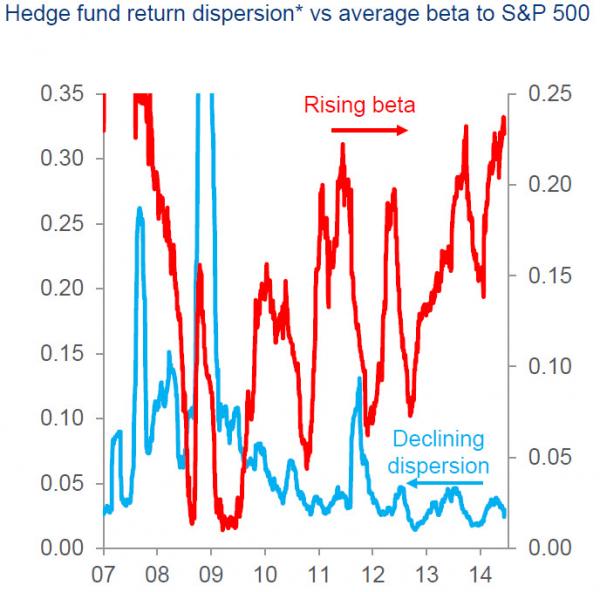

And the risk of hedge funds, despite providing unconscionable high returns during the housing bubble and the recession, has steadily been increasing.

And since banks started making these sorts of investments post-Glass-Steagall, their standard deviations have on average increased. A simple, non-causal relation I’m sure.

And that is precisely what is criticized in “Reconsidering…”: “a correlation between the proprietary trading activity and the losses certainly existed, but not a significant causal relationship” (34 No. 6 Banking & Fin. Services Pol’y Rep. 1, 3). Madison et al. instead say that the problem is in “supersenior” collaterized debt obligations (CLO’s). Blaming CLO’s is convenient for industry shills: “supersenior” CLO’s are not stratified into risk tranches, under the mistaken belief that properly construct CLO’s could not completely default. The problem with that belief: (1) quite a few CLO’s were not properly constructed (2) there was risk, and the banks hid it in undercapitalized bond insurers. In both these instances, you have causes of the collapse that are easy to atomize into the fraud or mistakes of a few “bad apples.” So if CLO’s are the main problem, what is Madison et al.’s solution? Capital requirements. In 2004, the S.E.C. allowed the largest broker-dealers to apply for exemptions. Because that exemption is still in place, it gives the more conservative critics of the recession a solid campaign target to obfuscate their agenda to chip away at Dodd-Frank piece by piece. The Financial Crisis Inquiry Commission Report (FCIC) does talk about how thin capital was an important factor:

In the years leading up to the crisis, too many financial institutions, as well as too many households, borrowed to the hilt, leaving them vulnerable to financial distress or ruin if the value of their investments declined even modestly. For example, as of 2007, the five major investment banks—Bear Stearns, Goldman Sachs, Lehman Brothers, Merrill Lynch, and Morgan Stanley—were operating with extraordinarily thin capital. –FCIC Report pg. xix

But here are the problems: first, the bad apple theory finds no correlation between the indisputable direct actors of the crisis and actors subverting capital requirements through the 2004 exemptions. Not only was Bear Stearns, public “bad apple” enemy number one, within the current capital requirements, they also happened to be within the pre-2004 capital requirements as well. It turns out that leverage held by the investment banks was not the fault of the 2004 exemptions at all:

Leverage at the investment banks increased from 2004 to 2007, growth that some critics have blamed on the SEC’s change in the net capital rules…In fact, leverage had been higher at the five investment banks in the late 1990s, then dropped before increasing over the life of the CSE program—a history that suggests that the program was not solely responsible for the changes. –FCIC Report pg. 153-154

The FCIC Report is being generous in saying “not solely responsible.” The capital requirement exemptions were not in anyway a major factor in the recession. They are merely a convenient scapegoat for the ill-informed and the zealots of free-market ideology. Such scapegoating is possible when the inability to see the forest from the trees pervades U.S. understanding of economics, or rather the inability to see the inherent contradictions of capital from the specific manifestations of it in various financial factors and instruments. As David Harvey points out, these contradictions are never actually solved, but rather moved around. His focus, as a geographer, is how this is done geographically, noting the examples of the U.S. to Brazil and the West to Greece. But geography is only one facet of place – financial investments, I would argue, are another. And this is the fundamental nature of capital; Karl Marx in Grundrisse states that-

…[capital] already appears as a moment of production itself. Hence, just as capital has the tendency on one side to create ever more surplus labour, so it has the complementary tendency to create more points of exchange…The tendency to create the world market is directly given in the concept of capital itself. Every limit appears as a barrier to be overcome. –Grundrisse pg. 334

And as finance experiences growth, it creates more points of exchange, which means more trades, in shorter time, with far more risk. Thus, the futility in “solving” the problems which caused the recession by imposing a single regulation that merely attempts to limit, not even growth itself, but the speed of growth. Madison et al.’s claim that short-term exchanges are not at issue is farcical. Bear Stearns demonstrates, about as clearly as one can get, that the singular function of lax capital requirements is not needed to engage in risky growth and, as Marx states in Grundrisse, such haphazard search for more points of exchange is intrinsic to capital itself.

But the Volcker Rule is hardly exempt from this criticism either, though built on slightly stronger foundation. As a Marxist myself I do not believe that there could ever be a set of regulations capable of preventing the uncontrollable swarming of capital. But while “every limit appears as a barrier to be overcome,” some barriers are far easier to overcome than others. The Volcker Rule certainly sets stronger, though not impermeable, limits to the reproduction of the conditions that created the recession than any single capital requirement ever could.

An apt analogy would be three “average people” in a race against one another. One runner is given a track that is simply a one mile line, and not given any restrictions. The second runner is given an identical track, but told “You can only run at 7 mph at any given time. But we will only check your speed once in the race, and will give you 30 seconds to slow down if you’re over the limit.” The last runner is given a labyrinth where the correct path is one-mile long, but allowed to run as quickly as they want. The first runner and second runner will likely have identical times: the average one mile time of a person is 8:18, or about 7.22 mph. That additional 0.22 mph could easily be made up while the referees are not watching. The last runner will likely have the worst time. Unlike the second runner, the last runner has actual limitations to how they can run.

But the Volcker Rule itself contains a number of loopholes, most notably the convoluted (d)(1)(G) exception to certain activities around hedge funds and private equities or the provisions governing activities outside the United States in (d)(1)(H) and (d)(1)(I). The confidence of the banks themselves in the face of the impending implementation of restrictions this coming summer may indicate that they have found, or expect to find, a means of subverting the Volcker Rule. Regardless, the specific naming of proprietary trading, private equity, and hedge funds allows future financial instruments that can be defined outside of these while serving similar functions to be engaged with by banking entities. In other words, the Volcker Rule may not be a labyrinth as much as a fork, one path with a dead end and the other leading to the finish line. How effective it will be is far too dependent on a large number of circumstances for Leftists to be comfortable with it even in the short term, and that is not even counting the 13 proposed pieces of proposed legislation (a political analysis of their viability would take far too long to go into here, but worth noting nonetheless).

Another piece of proposed legislation could alter the Volcker Rule if enacted, and that’s Elizabeth Warren and John McCain’s 21st Century Glass-Steagall Act. While hardly the means of putting an end to any triggering of mass dispossession by recession, the strict separation of banking activities significantly reduces the effect of risky financial actors on commercial banks, as well as ending poor assessments of risk that give undue power to diversification of investments regardless of the kind of investment. Further, for those of us interested in pushing for worker cooperative banking, nationalized banking, public banking, etc., a Glass-Steagall reinstatement would decrease the short-term competitive edge commercial banks have by investments too risky for small, community or municipal public banks to take on. While it only has six co-sponsors and the bill’s prospects are rather grim, the idea has enough popularity to stay in the media, albeit with a far less Leftist lens than I give it.

But we can all act on this issue immediately in two simple ways. The first is to refuse the resignation to commercial banks being above the law and regulation. To refute the rewriting of history to claim that the recession was not caused by a lack of regulation. To state plainly that the banks got bailed out and we got sold out, and that we cannot accept that as business as usual. And the second is to divest. Divest from predatory financial institutions. Divest from the big commercial banks that have profited from investing in those institutions. Stop making investments with the sole goal of profit, and start taking conscious measures to avoid the schemes that hurt people of color, women, and the working class. To do so completely is impossible: there is no ethical consumerism when capital only exists from the surplus value extracted from labor. But to change that larger problem requires rebuilding society in a way that will be made far more difficult if our communities are torn apart by increasingly brief gaps between recessions.

Read Part 2 on Orderly Liquidation Authority here.

Support my work through a $1 or $5 donation!

The third part of this

The third part of this

A recent event has led me to make

A recent event has led me to make  Most Leftist groups face a fairly unwieldy task of challenging a whole range of complicated issues with far less funding and time than their conservative counterparts. That is compounded by an overall focus on trying to prevent individual people from suffering which, while a noble endeavor,

Most Leftist groups face a fairly unwieldy task of challenging a whole range of complicated issues with far less funding and time than their conservative counterparts. That is compounded by an overall focus on trying to prevent individual people from suffering which, while a noble endeavor,